In 2014, CVS Health, a major US retail pharmacy chain, stopped selling tobacco products in all of their stores, in spite of the significant contribution that these products made towards sales. The following year, the company left the U.S. Chamber of Commerce to protest lobbying against tighter tobacco regulation.

In Germany, CEOs are also increasingly involved in shaping the broader context of business. In July 2017, Peter Terium, CEO of Innogy (ex- renewable energy branch of RWE) launched the #We4Europe coalition for “an open, united and strong Europe” as a reaction to growing anti-EU sentiment. The coalition was joined by many high-profile German companies such as Thyssenkrupp, Volkswagen and Lufthansa.

These are examples of corporate statesmanship. There is now a strong case for CEOs to take a bolder role in public affairs.

What is corporate statesmanship?

In politics, statesmanship designates the skill of managing state affairs, while a statesman is “a wise, skillful, and respected political leader”.[1]Source: Merriam-Webster dictionary Statesmen place the common good above their own interests and actively work to shape the context.

Because they control wealth, the fate of employees and choices on their products, CEOs are influential political players, whether or not they realize or exercise their power. They can therefore realistically aspire to statesmanship by acting for the common good, and not just the immediate interests of their companies.

We can define corporate statesmanship as the action of a company, and in particular of its CEO, to intervene in public affairs to foster collective action in support of the common good beyond the scope of their enlightened self-interest.

Society is facing unprecedented challenges

Social stresses abound and 2018 may well prove to be a moment of truth for CEOs, especially in the US, where companies will be under greater scrutiny because of tax reductions and regulatory relief.

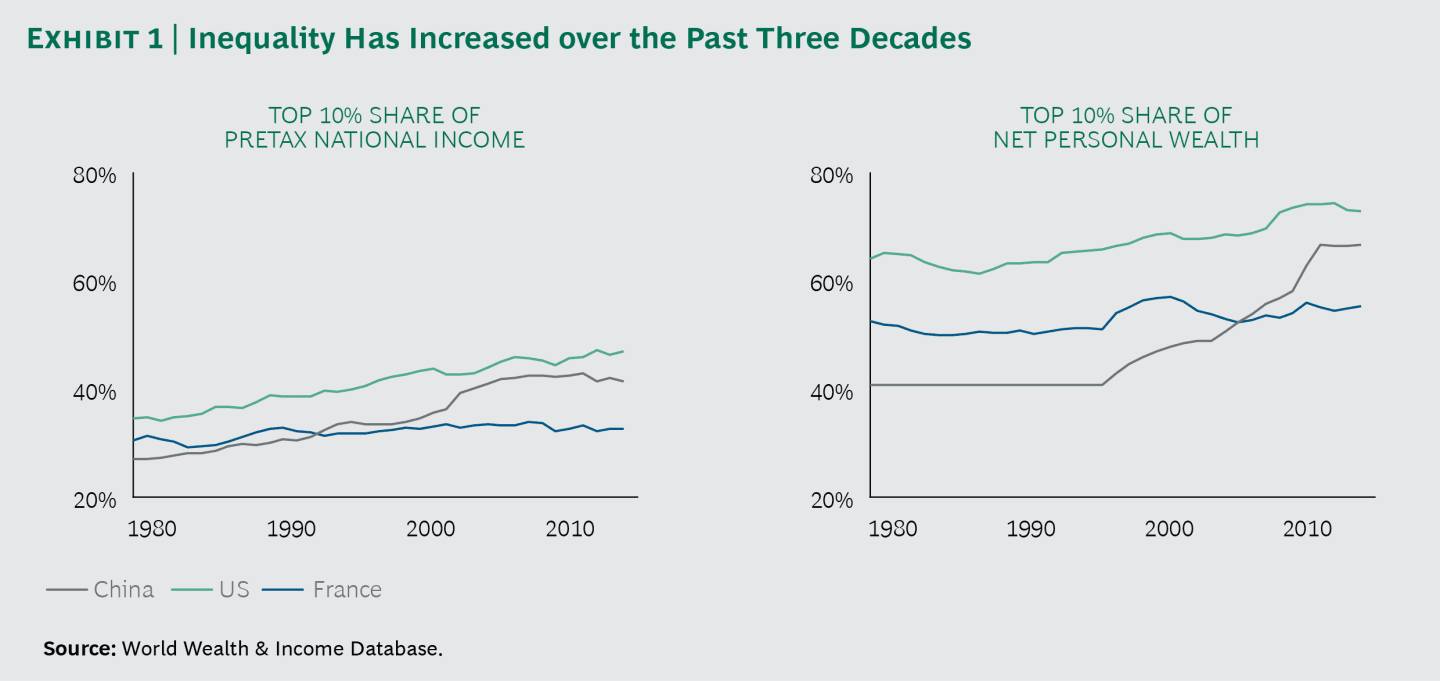

The societal challenges we face are well-known. Inequalities have been strongly increasingly over the last 3 decades, although slower in Europe than in the rest of the world (figure 1).

The rise of a new protectionism is part of a backlash against globalization that is starting to impact business itself.

The capacity of technology to foster progress and economic development is being questioned. The development of AI and robotization are increasingly feared as threats to employment rather than drivers of opportunity.

Another major challenge is the declining ability of the public sector to protect public goods, and in particular the environment. The latest research shows that despite the technologies at our disposal, we will likely miss Paris climate targets. And a growing world population will place further stress on the environment: irreversible biodiversity losses, water scarcity, lack of arable land and pressure on protected areas all seem likely to intensify.

Traditionally, we would expect governments to address these issues. In most of the world, there is a historic division of roles where corporations drive economic activity while governments take care of the common good.

As a result, there is an understandable reluctance for firms to get involved in public affairs. And allowing companies a stronger role can certainly create conflicts of interest, akin to having the fox watch the hen house. Numerous historical cases of failures of self-regulation support this view. Alan Greenspan, former Chairman of the Federal Reserve, famously claimed: “I made a mistake in presuming that the self-interest of organizations was such that they were best capable of protecting their own shareholders”.

Governments won’t necessarily be able to address the challenges

There are strong reasons to believe that governments may not be in a position to address some of today’s challenges by themselves.

The scope and scale of some of the challenges are arguably too broad even for large individual states, while weakening global cooperation reduces the chances for collective action. Political cycles limit the ability of governments to address long-term issues. On average, there are 1.7 national elections every quarter in the EU, undermining the continuity needed to attack long term challenges. And increasing political polarization further limits opportunities for public action in many parts of the world.

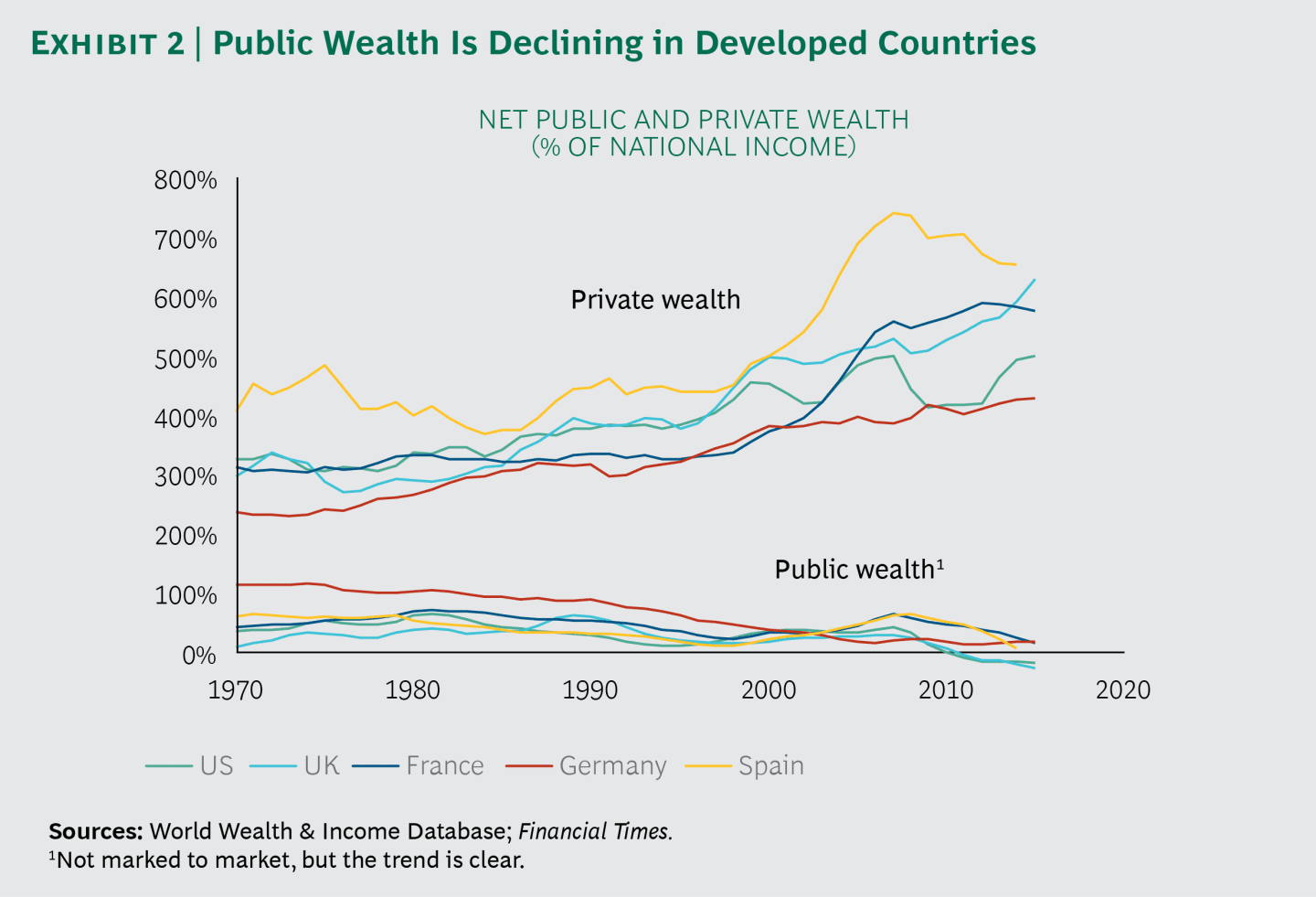

Financial pressures also contribute to institutional fragility and constrain public action. The welfare state is reaching its limits in developed countries, driven by aging and a shift from public wealth to private capital (figure 2).

The picture becomes even more complex if we consider the compounded effect of these various challenges. For instance, a 2016 article demonstrates that “Income inequality has a large, positive and statistically significant effect on political polarization”.

As a result of these and other factors, confidence in governmental institutions is falling, which further reduces the power of states as change agents. According to the Pew Research Center, public trust in the government is near historic lows in the US. Only 18% of Americans today say they can trust the government to “do what is right”.

The case for stepping up

Given this, there is a strong case for corporations to step up their statesmanship.

Of course, many CEOs fear that a more public role might generate exposure to backlash, especially in a context of increasing skepticism towards institutions. According to a recent survey, while 38% responded that CEOs have a responsibility to speak out on controversial issues, 36% said they believe the top reason for CEO activism is “to get media attention” (HBR, 2016).

As in post-war Japan, corporations are economic giants but still political dwarfs. Leaders tend to focus on immediate business problems: only 2% of board directors see “the role of business in society” as having the greatest effect on their company over the next 12 months (NACD 2017–2018 Board Survey).

However, the risk of acting needs to be balanced against the risk of inaction. If they stay passive, firms could soon find themselves damaged by an environment of escalating political risk. Ultimately, consumers and society have the power to sanction or restrict the freedom of action of global corporations. Regardless of political inclinations, corporate leaders have a common interest in preserving the game of business and defending the drivers of growth, like technology and globalization.

Corporations don’t just have a self-interest to step up, they are also well positioned to do so. Fundamentally, they are effective at problem-solving. They can act globally, in contrast to national governments. They have access to access to resources, skills and technology. Profits and cash accumulation are at historical highs, especially in the United States with recent corporate tax reform, so there is a large margin for action right now. As the influence of business has grown so has its ability to shape the provision of public goods essential for market stability.

Ultimately business cannot succeed if societies fail. Global markets need global rules for business to play its proper role in creating wealth and spreading solutions.

Statesmanship is more than CR

The business community is increasingly stepping up on sustainability and Corporate Responsibility (CR), not least because of growing evidence of a positive link with financial performance. The recent ascendancy of sustainable investing, enabled using tools such as the Arabesque S-Ray,will further accelerate good practices across industries. This alignment of finance with CR will could make a significant contribution to society in terms of environmental stewardship, workplace conditions and good governance.

In essence, CR is a long-term maximization of self-interest in which companies ensure that they don’t damage themselves by undermining their own environments. CR is fundamentally about individual action, in ways which are compatible with common interest — in other words, “doing well by doing good” within an existing policy framework.

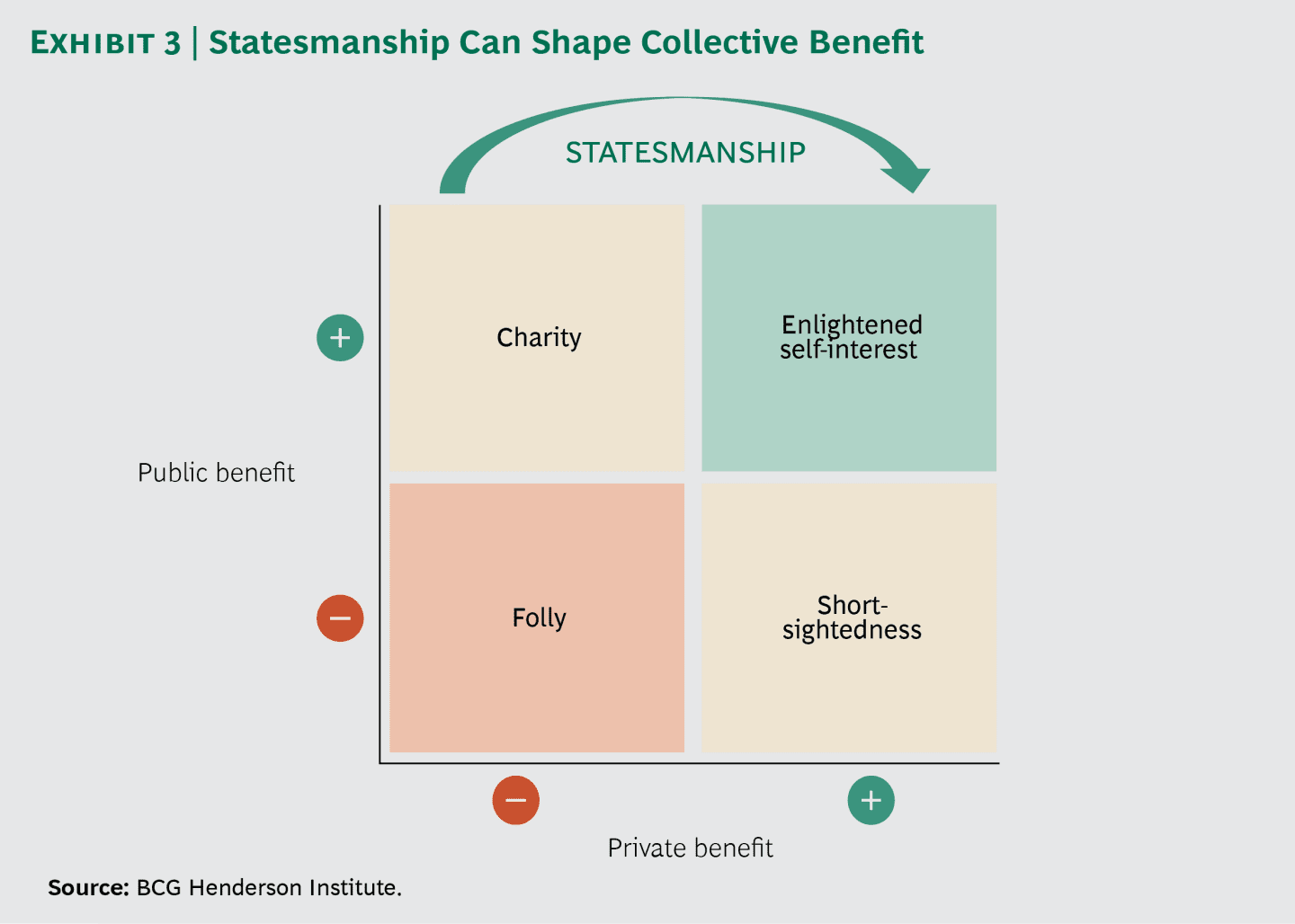

By contrast, statesmanship goes a step further. It is about shaping the policy framework to advance the public and private interests and changing the game by influencing the collective will (figure 3). It tackles problems that can’t be resolved through the enlightened self-interest of individual companies. The Prisoners’ Dilemma is used in economics to describe the situations where without collective action all actors tend to undermine each other, which leads to suboptimal individual outcomes. In other words, because each company follows its own path, an entire industry or economy ends up hurting itself. In those cases, statesmen are needed to foster cooperation and lift everyone to a better equilibrium by changing the nature of the game.

Cybersecurity is a good example of a prisoners’ dilemma in business. Everybody has a direct interest in seeing their data protected: citizens, consumers, producers and creators alike. But nobody has an interest in investing too much in the security of their own systems. This leads to systemic vulnerability, where breaches of security caused could have a negative impact on all and literally take down companies.

The path to statesmanship

1. First, be a good citizen

A good statesman has to be a good citizen. Gaining trust requires behaving responsibly, and being perceived in this light by other stakeholders. Maximization of Total Shareholder Return (TSR) within given legal boundaries is not enough. Leaders need to define clearly a human purpose, the higher social goal which their corporation serves, and ensure that their impact is compatible with that purpose. And they need to ensure that their own operations are based on values and a commitment to integrity.

A good start is the assessment of your firm’s economic, social, environmental and political impact. To this end, BCG recently developed a new metric called Total Societal Impact (TSI), which can be used to lay the foundations for a sound sustainability strategy.

2. Understand and protect the rules of the game

Above being a good citizen, statesmen need to protect the rules and institutions which guarantee balance in society. Companies benefit from a “license to operate” from society. Statesmen understanding the underlying conditions of the game, and the lines that cannot be crossed without jeopardizing their license to operate.

For example, Allergan CEO Brent Saunders acknowledged that “The health care industry has had a long-standing unwritten social contract with patients, physicians, policy makers and the public at large”. Perceived breach of that contract could threaten the entire industry: “As the focus on price has heated up, the innovation ecosystem has come under assault, and it is fragile”.

To protect the game, Allergan offered a new “social contract” to patients, with a focus on responsible pricing. The company then argued for industry-wide action, along with other CEOs. Recent data suggests Allergan’s commitment on pricing may be shaping de facto industry norms.

3. Bolster government

To play the game of business, companies need a fair set of rules and a referee. We tend to forget the value of regulation and criticize overregulation, but the rule of law is a basic condition for economic development. African fintech CEOs have been calling for regulatory actions to prevent fraud and facilitate the development of the industry. “Regulations have a huge role to play in ensuring the fintech industry becomes bigger and better,” said SimbaPay CEO Nyasinga Onyancha

In developed economies too, corporations should support the role of the state as regulator and referee. Elon Musk’s letter calling for the banning of autonomous weapons, which select and engage targets without human intervention, is an example of embracing regulation for social good. His letter clearly states that this about protecting the game and preventing: “a major public backlash against AI that curtails its future societal benefits”.

4. Support smart regulation

Empowering governments is a first step, but corporate leaders also need to propose and support smart regulations to preserve social balance. A case in point is the financial industry, which is highly complex and interconnected. It shares many features with biological systems, where all actors benefit from the ecosystem. In such situations, actors that over-stretch the system by systematically maximizing their private benefits may provoke collapse that is ultimately detrimental to their own interests.

Because statesmen are aware of those dynamics, they address a wider responsibility and support regulations that underpin a sustainable future for their industry. ExxonMobil’s CEO Darren Woods realizes that “growing demand creates a dual challenge: providing energy to meet people’s needs while managing the risks of climate change”. Therefore, in his first blog post as CEO, he advocated a “uniform price of carbon applied consistently across the economy” as the smartest way to meet that dual challenge.

5. Oppose injustice

When confronted with situations that are obviously unfair, the right response of the statesman is to take action. As Elie Wiesel put it, “We must take sides. Neutrality helps the oppressor, never the victim”.

Assessments of “right” and “wrong” should be informed by universal values and principles that we have learned from history.

To use the framework developed by economist Albert O. Hirschman, there are 3 ways to act:

- Exit, or refraining from participating in certain markets that don’t meet standards,

- Loyalty, or remain silent where general interest prevails (but a chosen silence rather a silence by default — the decision can be explained later if necessary),

- Voice, public communication of disapproval.

“Voice” may generate exposure for a corporation. One option for CEOs to mitigate such a risk is to distinguish their opinions as citizens from those of their companies. Sergey Brin attended demonstrations in his personal capacity, not as President of Google. This can be a good way to respond without the company appearing to customers and stakeholders as politically biased.

6. Take the lead

The major issues of society are well-known. Sometimes even the solutions are obvious but political, social or economic conditions prevent those solutions from being implemented. Statesmen do not use this as an excuse and will instead take the lead and demonstrate that action is possible.

In the cybersecurity example mentioned above, Google built a group of hackers called Project Zero, in order to identify and address digital threats, with a focus on the software made by other companies. This is a tangible way for Google to show that it takes responsibility for the overall stability of the system.

7. Shape and join horizontal coalitions with other companies

Leadership and exemplification are meant to trigger collective action. For businesses, the rationale for engaging with others is not just about maximizing impact. Acting together with other industry players is also a way to ensure that the conditions of competition remain fair and equivalent for all.

CEOs can help form and shape such coalitions to realize their values. There are many ways to do this, but the UN Global Compact has been decisive in providing a unified framework for business coalitions across a wide array of sustainability principles based on universal values.

In a particularly striking example, 400+ companies including Microsoft, Adidas and Sony have committed to being climate neutral, i.e. to minimize their greenhouse gases emissions, and compensate for unavoidable emissions. Businesses should not be afraid to engage with other types of actors too: the climate coalition also includes individuals, cities and non-profits.

8. Shape vertical coalitions with investors

CEOs have a direct legal responsibility toward their shareholders. This is often used as an argument for business leaders to remain within the strict limits of their assumed mandates, and focus on the maximization of TSR. However, there are now many examples of investors pressuring leaders to take a stand on societal issues. In January 2018, two Apple investors pressured the company to address concerns over smartphone addiction. They requested management to better assess the mental health effects on children, and take appropriate action.

Neglecting this type of pressure might come at a high price. Norway’s pension fund, the world’s largest sovereign wealth fund, which owns on average 1.3 per cent of every single listed company on earth, decided to divest from oil and gas as part of a climate change strategy.

Sustainable investing enabled by technology and big data analysis, as advanced by firms like Arabesque, is making investors increasingly powerful allies for corporate statesmen in addressing social challenges.

9. Build narratives

It is often impossible for even informed citizens to know all of the facts, which are in any case often disputed, especially in the case of controversial social issues. People understand reality individually and collectively through stories. Statesmen exert influence and shape minds and foster action through narratives. CEOs need to explain why they believe what they believe and advocate for it by building understandable and compelling narratives, which not only stand up to scrutiny but which can create alignment and support.

Lyft co-founder John Zimmer is well aware of a risk of backlash against new forms of mobility. So he tries to argue that car sharing is more than a business, that it has a huge impact on the design of cities, with “tremendous implications on global economics, health, social equality, the environment, and overall quality of life”. This puts the company in a better position to shape the future of the industry.

Conclusion

Business leaders need to face the inconvenient truth that some aspects of collective welfare can’t always come from individual maximization efforts, even enlightened ones. They require the “technology of leadership” to solve the prisoners’ dilemma of non-cooperation leading to poorer outcomes for all.

Corporations that lead will be trusted more and accepted as a partner by governments and citizens. Actions will foster more actions, and 2018 could well be a foundational year for corporate statesmanship.